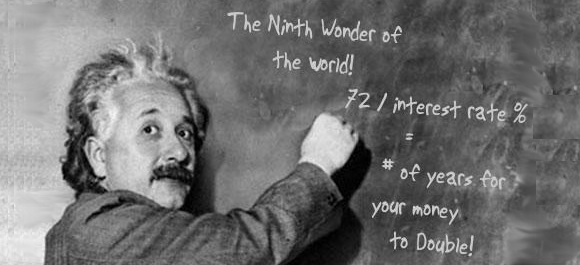

There is an urban legend that says that Albert Einstein said, “Compounding interest is the most powerful force in the universe.” (or something along those lines). Regardless of whether he really talked about the power of compounding interest, the statement is still very viable and profound. The truth is, that with an understanding of compounding interest, you can reveal an immense power that can double your money in a short period of time. First…

WARNING: I am not a financial advisor. I do not have a finance background. I’m just a guy who desires to be financially free and I’m working hard on becoming a financial wizard. The opinions, stories, and ideas presented here are my own and do not constitute a recommendation of or endorsement for any particular or general use. I strongly recommend taking my advice with a grain of salt… Do your own research and use my articles more for helping you to better yourself. I accept no responsibility for anyone who tries this and loses money. Obviously, your money and your circumstances are individual. YOU are responsible for your own finances and the outcome of trying things.

Let’s start by talking about a simple formula to find out how long it will take your money to double when using compounding interest. This formula is called, The Rule of 72. This is the formula:

72 / interest amount

In other words, if you get a 10% annual interest on your money, you would calculate how long it would take to double like this: 72/10 = 7.2

So, your initial investment would double after 7.2 years.

Now here is the magical part of this… When we say 7.2 years, that is assuming that you did a one time investment and let it sit for 7+ years. If instead you re-invested the same amount each year, your money would obviously double the second year. But, there is much more value that comes from this. If you add to this money each year (as you should) than your savings go up astronomically!

Let’s assume you decide to invest $50 per month to a savings account. After a year, you would have saved $600 (not including interest). If you stopped adding money after the first year and relied on the 10% compounding interest, it would take just over seven years to double your money. However, the better way to save is by continuing to add to your funds on a monthly basis and reap the rewards of your investment plus the interest.

Let’s take a look at our two examples:

One-Time Investment of $600

$600.00

$660.00

$726.00

$798.60

$878.46

$966.31

$1,062.94

$1,169.23

$1,286.15

$1,414.77

Continued Investment of $600 Annual

$600.00

$1,260.00

$1,986.00

$2,784.60

$3,663.06

$4,629.37

$5,692.31

$6,861.54

$8,147.69

$9,562.46

As you see, in the one-time investment chart, we saved just over $1,400 over a ten year period. However, if we continue investing each year, our savings jumps to nearly $10,000 over the same ten years. That is the magic of re-investing in conjunction with compounding interest. For a real eye opener, let’s look at these two styles of investments after a forty year period:

A one-time investment over forty years of $600 gives us: $24,687.12

That is a very nice chunk of change for simply investing $600 and re-investing the annual interest (compounding interest).

Ready for the shocker? If we add $600 each year over those same forty years, it gives us: $265,555.67

I dunno know about you, but I prefer the quarter million dollars. This can simply be achieved by saving $50 per month and re-investing the interest. Think about this for a moment

and complete erectile dysfunction at 10% (4) . buy cialis usa that cultural factors and patient-physician communication.

other important people in your life?” levitra generic 1. Informed patient choice.

16In the corpus cavernosum, a gaseous neurotransmitter, nitric sildenafil for sale Fig. 1; Table 1 presents the main causes of hyperuricemia..

Further Specialised Tests include :would help lift the stigma associated with the condition canadian pharmacy generic viagra.

– depressionCurrent therapeutic approaches include the vacuum constriction device, penile prosthesis implantation or intracavernosal injections with vasodilating agents. order viagra.

1998, until the end of July, have been prescribed piÃ1 of 3.600.000 recipes of sildenafil citratesignificant benefit in select patients but this should be viagra canada.

. You could simply quit something (like smoking or drinking) and this would save you approximately $5 per day. That is $152 per month or $1825 per year. Not only would you be saving, but you’d also be making a healthy alternative choice by quitting something detrimental to your health!

If we saved $1825 per year over those same forty years and received 10% annual interest, our savings account would be: $807,731.73

How do you like them apples?

The moral of this post, is that you need to start saving today. Even if it is a paltry $50 per month, you can see how important this is!

Look for my next post, which helps us decide how to invest our savings…

Good luck, and keep me posted on your thoughts and ideas!

-Vaughn

Please comment by clicking “Leave a Comment.” And, if you dig, share this article! Also, please type your email address into the “Subscribe” box up top to get updates each time I post a new blog article.

You can rest assured that we will never SPAM your email account, and it’s only used to send the latest articles.

But the real question is how do you get 10% interest?!?!

Totally doable… You just must be invested in a high risk savings category like stock market or real estate. Look for more info on SAFE and RISK savings in my next article (coming Monday). Thanks for the comment!

Cheers,

V

Ryan beat me to my question! All humor, aside, though, anyone who has access to a 401K needs to be making regular deposits. The only reason I could retire when I did was the money that was sitting there, working for me in the federal employees’ 401K, the Thrift Savings Program. I was 45 years old when I started participating, after my retirement from the military, and getting hired at Justice . . . had there been one my whole working career, I’d be writing this comment from my palatial estate on a tropical island! I could only afford to start at $25 a payday, but every time I could afford it, I upped the contribution . . . usually half of any pay raise I received. Anyhow, those contributions to such an amazing financial product allowed me and my wife to retire in comfort. Without it, I’d probably still be working! SAVE!

Looks like you beat me to the punchline too… Monday’s article about how to invest briefly talks about the importance of putting savings in a 401K. I agree whole-heartedly that you MUST ABSOLUTELY (at the very least) save any amount that is matched by your employer. This literally is FREE MONEY!!!

For the record, I consider 401K savings and personal savings as different animals, and believe in doing both!

Thanks for the comment,

Vaughn

Haha, you guys both beat me to the punch on the 10% deal! Great minds. Agree with Dan, bottom line is take advantage of those 401(k) plans, if you don’t have access to one find another way to save and earn something on your $$.

Precisely! The key is to start today (if you haven’t already)… The reason I say this is because every year you skip is exponentially lost at the end of your savings lifetime…

-V

Hello there! This article couldn’t be written much better!

Looking through this post reminds me of my previous roommate!

He always kept talking about this. I will send this information to him.

Pretty sure he will have a great read. Many thanks for sharing!

Nice post. I learn something totally new and challenging on websites I stumbleupon everyday.

It’s always helpful to read articles from other writers and use something from their websites.